How Enterprise DXPs are Redefining Financial Loyalty in Saudi Arabia

Table of Contents

- 1. Introduction

- 2. The New Standard for Saudi Finance

- 3. Why "Good Enough" is a Risk

- 4. From Infrastructure to Impact

- 5. Aligning the Enterprise Through Shared Capabilities

- 6. Navigating the SAMA Landscape With Confidence

- 7. Financial Use Cases Across the Vertical

- 8. Selecting Your Foundation for Growth

- 9. The iSpectra Partnership for Financial Excellence

- 10. Conclusion The Cost of Inaction

1. Introduction

In Saudi Arabia's rapidly evolving fintech landscape, loyalty in the financial sector is no longer defined by the size of a physical branch network. Today, it is won or lost in the milliseconds it takes for a mobile app to load, the relevance of a push notification, and the ease with which a customer can apply for a mortgage using digital financial services.

As Vision 2030 accelerates the Kingdom toward a digital-first economy driven by financial technology innovations, the pressure on banks, insurers, and asset managers has shifted. It is no longer enough to simply offer digital services. They must deliver unified digital experiences and seamless customer experiences. This is where the Digital Experience Platform (DXP) becomes the most critical asset in a financial organization's architecture.

At iSpectra, we see a clear trend in Saudi's fintech ecosystem. Institutions that treat their digital presence as a collection of silos are losing ground. Those that treat it as a unified platform are not just surviving. They are defining the new standard of the Kingdom's fintech saudi landscape.

Back to top

2. The New Standard for Saudi Finance

The Saudi Arabian financial sector is undergoing its most significant transformation in decades. Driven by the Financial Sector Development Program (FSDP), the goal is clear. The Kingdom aims to increase the share of digital payments and non-cash transactions to 70%, foster financial inclusion, and cultivate a thriving fintech ecosystem.

For established banks and insurance providers, this creates a dual challenge. You must meet the rigorous security and data residency standards set by Saudi Central Bank (SAMA) while simultaneously competing with agile, digital-only challengers offering mobile wallets and other digital financial services.

A DXP is the foundation that allows you to bridge this gap. It is not just a Content Management System. It is an integrated suite of technologies designed to simplify how you create, manage, and deliver personalized customer experiences across every touchpoint, including web, mobile wallets, and physical kiosks. By adopting a platform-based approach, Saudi institutions can ensure they are not just complying with the present, but are scaling for a future that demands hyper-personalization in the digital payment ecosystem.

Back to top

3. Why "Good Enough" is a Risk

In Saudi Arabia's competitive market, relying on fragmented legacy systems is a strategic liability. When your customer data lives in one place, your content in another, and your transaction engine in a third, the user experience suffers.

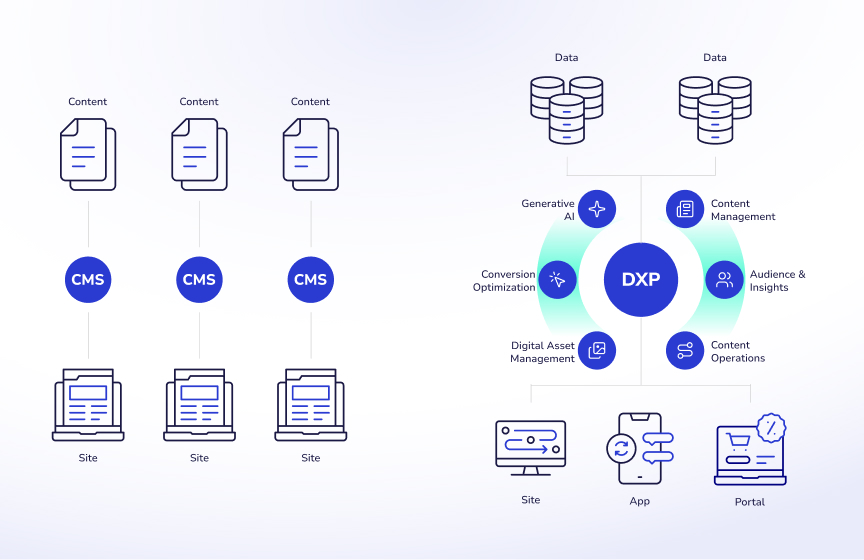

From CMS to DXP: A Critical Evolution

Many institutions still operate on a traditional Content Management System (CMS). While a CMS is effective for basic tasks like updating a blog or changing a landing page, it is fundamentally limited. A CMS manages content for a single website. In contrast, a Digital Experience Platform (DXP) is an integration hub.

A DXP unifies content management with APIs, customer data, and machine learning. While a CMS asks, "What can we publish?" a DXP asks, "Who is this customer, and what do they need right now?" For a Saudi bank, this means moving from a static homepage to a dynamic portal that recognizes a user's unique financial profile and provides a personalized customer experience.

Data Harmonization and Audience Intelligence

True loyalty is built on understanding. Most financial institutions struggle with data silos where the mortgage team does not recognize the long-term checking account holder. A DXP enables data harmonization. It connects disparate systems like your CRM, core banking system, and mobile analytics into a single "golden thread" of information to enable real-time payments and a unified customer experience.

This harmonization fuels audience intelligence. Instead of sending generic credit card offers to every user, the platform uses real-time data to identify specific segments. For example, it can recognize a high-net-worth individual who frequently searches for international travel insurance. The DXP then automatically prioritizes relevant wealth management content, increasing both trust and conversion.

Omni-channel Personalization at Scale

Modern Saudi consumers expect a seamless transition between channels. They might start a loan application on their mobile app or mobile wallet during a commute and want to finish it on a laptop later that evening.

Omni-channel personalization ensures the experience is continuous and consistent across digital financial services. A DXP serves as the central brain that orchestrates these interactions. It ensures that the "Welcome back" message, the pre-filled application data, and the personalized investment advice are identical across every touchpoint. This level of sophistication is what distinguishes market leaders from those just offering a digital presence in the digital payment ecosystem.

Back to top

4. From Infrastructure to Impact

A Digital Experience Platform is not merely a technical upgrade. It is a fundamental shift in how a financial institution creates value. When you move away from fragmented legacy systems, you bridge the gap between back-end capabilities and front-end expectations. At iSpectra, we guide our partners to focus on the outcomes that define market leadership in Saudi's fintech landscape.

Driving Growth through User Precision

In the world of Saudi banking and insurance, every interaction is an opportunity to deepen a relationship or lose a lead. By using a DXP to unify your data, you enable a level of precision that directly impacts the bottom line and enhances the customer experience.

Our implementation strategies are designed to deliver clear results. On average, our partners experience 5% more page views and 10% longer sessions. These are not just traffic numbers. They represent a more engaged customer who is finding the answers they need without friction. This engagement is the foundation for a 25% increase in online sales of digital financial services like mobile wallets. When the path to a personal loan or an insurance policy is simple, customers complete the journey rather than abandoning it.

The Power of Anticipation

Loyalty in the digital age is built on anticipation. When your platform remembers a user's preferences and suggests the next logical step in their financial life, the institution moves from being a utility to being a partner. This relevance drives a 24% increase in returning visits. Customers return to platforms that respect their time, understand their needs, and provide a personalized customer experience.

Redefining Operational Velocity

Perhaps the most significant impact of a DXP is the speed it grants to your internal teams. In a traditional setup, launching a new savings product or updating a policy document can take weeks of manual coding and testing.

A modern DXP architecture allows your organization to roll out updates 10 times faster. It provides a 5x greater ability to launch new products compared to legacy frameworks. This velocity is what allows Saudi financial institutions to remain agile in the fintech saudi landscape. You can respond to a new SAMA regulation or a competitor's move in days, not months, enabling real-time payments and rapid innovation in the digital payment ecosystem. This shift from infrastructure to impact ensures that your technology is an accelerator for your business rather than a bottleneck.

Back to top

5. Aligning the Enterprise Through Shared Capabilities

A successful digital strategy requires more than just a talented IT department. It requires a platform that enables every stakeholder to contribute to the customer journey. When a financial institution adopts an enterprise-grade DXP, it breaks down the walls between departments and allows teams to work toward a common goal of delivering exceptional customer experiences.

Empowering Marketing Teams

Marketing professionals in the banking sector need to be agile. They must be able to launch campaigns and adjust messaging without waiting for a developer's schedule. A DXP provides intuitive tools that allow marketers to design and deliver experiences that build trust and enhance the customer experience. With the ability to test different versions of a landing page or personalize content for specific demographics, they can drive loyalty through relevance.

Optimizing Operations Teams

Operational efficiency is about reducing the distance between an idea and its execution. By using a unified platform, operations teams can stay ahead of industry trends and changing customer expectations in the digital payment ecosystem. This architecture reduces the cost of maintaining multiple disparate systems. It allows the organization to scale its digital financial services offerings without adding significant overhead or complexity to the daily workflow.

Enabling Technology Teams

The role of the technology team shifts from maintenance to innovation. Instead of spending hours fixing integration errors between old software, they can focus on building customer-centric services. A DXP provides a robust foundation that supports organizational goals in an agile way. It allows for the quick creation of new digital solutions while ensuring the underlying structure remains stable and secure, enabling real-time payments and other financial technology innovations.

Back to top

6. Navigating the SAMA Landscape With Confidence

For any financial institution in Saudi Arabia, compliance is the non-negotiable baseline for operation in the digital payment ecosystem. The SAMA Cybersecurity Framework and data residency laws create a complex environment that requires intentional system architecture.

Security by Design

A DXP is not just a layer for the user interface. It is a secure gateway. Modern platforms are built with enterprise-grade security protocols that align with global and local standards. iSpectra ensures these platforms are configured to meet strict requirements while protecting sensitive financial data.

Access Control – We implement robust identity management to ensure only authorized personnel can manage the experience layer.

Encryption Standards – All data in transit and at rest follows high-level encryption protocols to prevent unauthorized access.

Audit Trails – The platform maintains detailed logs of every change and interaction to simplify the regulatory reporting process.

Managing Data Residency

The Saudi government is clear about where financial data must reside. One of the primary advantages of working with an experienced partner like iSpectra is the ability to deploy these platforms correctly in the digital payment ecosystem.

Local Cloud Deployment – We facilitate hosting on Saudi-based cloud providers to ensure all data stays within the Kingdom.

On-Premise Flexibility – For institutions with higher security needs, we provide support for internal data center installations.

Sovereignty Compliance – Our architectures are designed to satisfy the local data protection laws without sacrificing the performance of the digital platform.

Balancing Compliance and Innovation

The challenge for many Saudi institutions is the fear that strict regulations will slow down innovation in the fintech saudi landscape. A DXP solves this by separating the core banking data from the experience layer.

Agile Front-End Development – You can update your mobile app interface without needing to re-validate the entire core banking engine.

Rapid Response – The platform allows you to adapt to new SAMA circulars or regulations in days rather than months, enabling real-time payments.

Secure Testing Environments – We provide sandboxed areas where you can build and test new features safely before they go live for customers.

This strategic separation allows you to gain the freedom to innovate at high speed while keeping your most critical assets under the strictest protection in the digital payment ecosystem.

Back to top

7. Financial Use Cases Across the Vertical

Every branch of the financial sector has its own set of challenges. A DXP is versatile enough to address these specific needs by creating tailored journeys for different customer profiles and digital financial services.

Banking and Credit

Retail and commercial banking rely on high-frequency interactions. The goal here is to reduce the effort required for routine tasks while maximizing the opportunity for cross-selling digital financial services like mobile wallets.

Streamlined Applications – A DXP can use pre-fill data from existing accounts to allow a customer to apply for a credit card or a personal loan in just a few clicks.

Proactive Support – By integrating AI chatbots and self-service portals, banks can resolve issues before a customer ever feels the need to call a support center, enhancing the customer experience.

Wealth and Asset Management

In wealth management, the relationship is built on transparency and specialized knowledge. Customers in this segment expect a sophisticated digital experience that reflects their status.

Personalized Portfolios – Investors can access dynamic dashboards that show real-time performance and receive investment advice tailored to their specific risk tolerance.

Secure Document Sharing – High-net-worth individuals can safely exchange sensitive legal and financial documents with their advisors through a secure, authenticated portal.

Insurance

The insurance sector is shifting from a claims-based model to a prevention-based model. This requires constant and meaningful engagement with the policyholder to enhance the customer experience.

Simplified Claims Processing – Customers can upload photos and submit claims directly through a mobile app or mobile wallet, receiving instant status updates as the claim moves through the system, enabling real-time payments.

Educational Content – By providing articles and tools related to risk management and wellness, insurers can move from being an annual expense to being a valuable daily resource.

Back to top

8. Selecting Your Foundation for Growth

Choosing a DXP is a long term strategic commitment. At iSpectra, we guide our partners through the selection process to ensure the technology matches their organizational maturity and technical requirements. Gartner evaluates these platforms based on their ability to execute and their completeness of vision in the fintech saudi landscape.

Strategic Comparison Based on Gartner Insights

Gartner consistently recognizes the platforms iSpectra specializes in as leaders or strong performers in the enterprise space. Each has a distinct footprint in the financial services sector and digital payment ecosystem.

Liferay – Gartner frequently highlights Liferay for its strength in building complex, authenticated portals. For Saudi institutions, this means a platform that handles the intricate security layers required for wealth management and corporate banking. It is praised for its flexibility and ability to integrate with various legacy back end systems, enabling real-time payments.

Sitecore – Positioned as a leader for its deep focus on the customer journey, Sitecore is recognized for its advanced personalization engine. Gartner notes its ability to combine content, commerce, and data into a single view. This is the preferred choice for retail banks in the Kingdom that want to deliver high value, personalized offers in real time across digital financial services like mobile wallets.

Acquia – Built on the open source power of Drupal, Acquia is often cited for its agility and cloud native capabilities. Gartner points to its strong developer community and ease of use for marketing teams. For insurance companies with multiple sub brands, Acquia allows for the rapid deployment of new digital properties while maintaining centralized control in the digital payment ecosystem.

Matching Platform Strengths to Institutional Goals

The choice between these leaders depends on your primary objective in the fintech saudi landscape. If the focus is on a high security client portal for high net worth individuals, Liferay offers the most robust framework. If the objective is to dominate the retail market through aggressive digital marketing and lead conversion across channels like mobile wallets, Sitecore provides the necessary tools. For organizations that value speed, modularity, and an open architecture, Acquia stands out as the most adaptable choice for financial technology innovation.

At iSpectra, we do not just recommend a platform. We analyze your current architecture and your Vision 2030 objectives to ensure the foundation you choose today can support the scale you need tomorrow in Saudi's digital payment ecosystem.

Back to top

9. The iSpectra Partnership for Financial Excellence

AA platform is only as effective as the architecture behind it. At iSpectra, we do not simply install software. We design and deliver comprehensive digital ecosystems that are purposely built for the unique demands of the Saudi financial sector. Our expertise allows your institution to move from complex legacy environments to streamlined, outcome-driven platforms.

A Proven Track Record with Leading Institutions

iSpectra is trusted by leading financial institutions to navigate their digital transformation journeys in the fintech saudi landscape. We have established ourselves as a go-to reference in the Kingdom by helping organizations modernize their infrastructure while strictly adhering to the SAMA Cybersecurity Framework. Our deep understanding of the local digital payment ecosystem ensures that our partners do not just implement technology, but achieve measurable strategic objectives.

Guidance from Design to Delivery

We believe in a partnership that begins with strategic clarity. Our team works with your stakeholders to define the technical requirements that will support your business goals. We ensure that every integration point and every user journey is designed with intentionality. This reduces friction for your customers and complexity for your staff.

Scaling Without Friction

As your institution grows, your digital platform must be able to grow with it. We focus on building architectures that support scale. Whether you are expanding your service offerings or managing a surge in digital transactions, the foundations we build remain stable. We enable you to remove barriers to action, allowing your teams to innovate and deploy new features with confidence in the digital payment ecosystem.

Local Expertise with Global Standards

Operating in Saudi Arabia requires a deep understanding of local market dynamics and regulatory expectations in the fintech saudi landscape. We combine our global technical standards with a local perspective. This ensures that your DXP is not only world-class but also culturally relevant and fully aligned with the Saudi financial ecosystem.

Back to top

10. Conclusion The Cost of Inaction

The window of opportunity to define digital leadership in the Saudi financial sector is narrowing. As Vision 2030 continues to reshape the economy, the institutions that will thrive are those that view digital experience as a core strategic pillar rather than a technical necessity.

The Competitive Gap

Choosing to delay the move to a unified Digital Experience Platform carries a significant cost. Every day spent with fragmented systems is a day where your competitors are gaining a deeper understanding of your customers. Without the data harmonization and speed that a DXP provides, you risk falling behind the expectations of a tech-savvy generation of Saudi consumers demanding digital financial services like mobile wallets.

The Regulatory and Market Reality

Inaction does not just lead to lost market share. It creates tangible risks for the organization in the digital payment ecosystem.

Risk of Non Compliance – Operating on legacy infrastructure often makes it difficult to implement the latest security patches or data residency requirements. This can lead to significant SAMA penalties, including heavy fines and the potential suspension of specific digital services.

Loss of Trust – A single data breach or a prolonged service outage caused by outdated architecture can damage a brand's reputation for years.

Operational Stagnation – If your team is stuck maintaining old code instead of launching new products, you are effectively granting your competitors a head start in the race for the next generation of Saudi capital and financial technology innovations.

Secure Your Market Position

The transition from infrastructure to impact is the path to long-term loyalty and revenue growth in the fintech saudi landscape. By partnering with iSpectra, you gain the clarity and the capability needed to navigate this evolution.

Deliver Unified Journeys – Provide a consistent customer experience across all banking and insurance touchpoints.

Achieve Compliance – Ensure your digital presence is built on a foundation that respects all local regulatory frameworks in the digital payment ecosystem.

Enable Rapid Innovation – Launch new digital financial services and updates with the speed required by a modern economy, enabling real-time payments and financial inclusion.

The future of Saudi finance is being built on unified platforms. The question is no longer whether you need a DXP, but how quickly you can deploy one to protect your market share, avoid regulatory friction, and enable your future growth in the fintech saudi landscape.

Build Your Future-Ready Digital Experience Platform with iSpectra

The path to digital leadership in the Saudi financial sector requires a partner who understands the balance between innovation and regulation in the digital payment ecosystem. Do not let legacy systems limit your institutional growth or risk your compliance standing.

Contact iSpectra today to schedule a strategic consultation. Let us help you design a DXP architecture that secures your market position and delivers the outcomes your stakeholders demand in Saudi's fintech landscape.

Back to top