Open Banking’s Impact on the Saudi Financial Ecosystem in 2025

Table of Contents

- The Rise of Open Banking in 2025

- How Open Banking Has Evolved

- Open Banking in Saudi Arabia 2025

- Players in KSA’s Open Banking Growth

- How AI & APIs Impact Open Banking in 2025

- How Open Banking is Changing the UX

- Security & Compliance Challenges in 2025

- Open Banking vs Traditional Banking

- Future Trends and Predictions

- The Future of Open Banking in Saudi Arabia

The Rise of Open Banking in 2025

Saudi Arabia's financial sector is undergoing a massive transformation. Open banking is no longer just an innovation—it is a necessity.

With fintech adoption soaring, and the Saudi government pushing for a 70% non-cash economy by 2025, digital financial services are becoming the norm.

Banks, fintech startups, and third-party providers (TPPs) are leveraging AI, API integrations, and blockchain to create a seamless and secure financial ecosystem.

Back to topHow Open Banking Has Evolved

Before 2022:

Traditional banking models dominated with limited financial service accessibility.

APIs existed but weren’t widely utilized for consumer applications.

2022-2024:

SAMA introduced the Open Banking Framework, enabling Account Information Services (AIS).

Fintechs gained access to user-permitted financial data, boosting digital financial services.

Growth of neobanks & digital-only banking solutions began reshaping Saudi Arabia's banking sector.

2025 & Beyond:

SAMA’s 2024 expansion of Open Banking now includes Payment Initiation Services (PIS).

AI-driven financial services are leading to hyper-personalized user experiences.

Security concerns drive stronger regulatory compliance and fraud prevention efforts.

Back to top

Open Banking in Saudi Arabia 2025

Saudi Arabia is now a regional leader in open banking adoption, with more than 600,000 customers onboarded to digital-only banks within two months of their launch.

Fintech Market Growth:

- The Saudi fintech sector is projected to reach $1.5 billion in 2025 (SDK Finance).

- A 37% increase in fintech companies since 2024.

Regulatory Advancements:

- The Open Banking Framework (2024 Update) introduced standardized PIS protocols to enable seamless transactions.

- Saudi Central Bank (SAMA) is ensuring compliance & security in API-driven transactions.

Back to top

Players in KSA’s Open Banking Growth

Leading Banks

National Commercial Bank (NCB) – Driving advanced API-powered financial services.

Al Rajhi Bank – Innovating with AI-driven customer experiences.

SABB (Saudi British Bank) – Early adopter of secure open banking APIs.

Top Fintech Innovators

Lean Technologies – Leading financial API provider fostering fintech-bank integrations (WhiteSight).

Tarabut Gateway – Powering next-gen personal finance solutions through open banking APIs.

STC Pay – Expanding digital wallet functionalities via secure API integrations.

Back to top

How AI & APIs Impact Open Banking in 2025

Artificial Intelligence and API-driven automation are redefining how users interact with financial services.

Personalized Banking – AI is creating tailored financial recommendations based on spending habits.

Seamless Transactions – Open APIs allow real-time payments and digital onboarding.

Fraud Detection – AI-powered risk assessments & security checks ensure safer transactions.

Ready to integrate AI-powered financial services?

Back to top

How Open Banking is Changing the UX

Instant Access to Financial Data – Users can securely connect banking apps to third-party services.

Faster Payments & Transfers – Open APIs allow seamless money movement.

Better Loan & Credit Decisions – AI analyzes financial health in real-time, providing personalized loan options.

Enhanced Security – SAMA’s 2025 compliance framework protects consumer data & transactions.

Back to top

Security & Compliance Challenges in 2025

With greater access to financial data, security remains a major priority.

SAMA’s Open Banking Framework (2024 Update) introduces higher compliance standards.

Stronger KYC & fraud prevention protocols are in place.

Multi-Factor Authentication (MFA) is now mandatory for open banking transactions.

Back to top

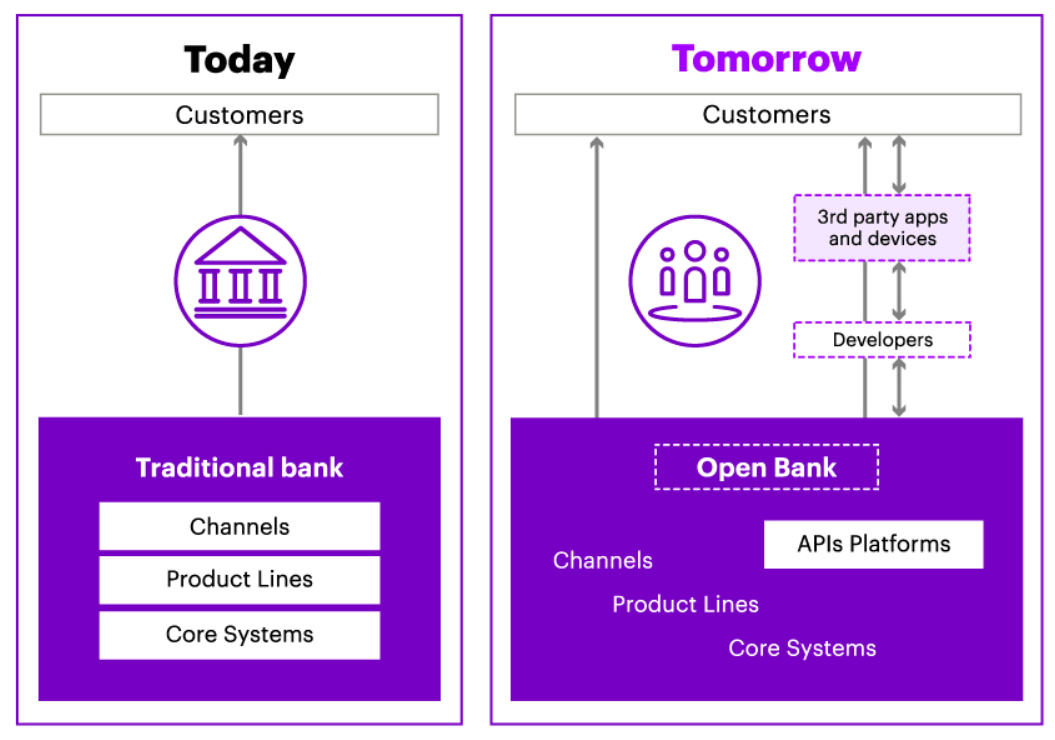

Open Banking vs Traditional Banking

| Feature | Traditional Banking | Open Banking 2025 |

|---|---|---|

| Financial Data Access | Limited | ✅ Full consumer control |

| Transaction Speed | Slower | 🚀 Instant transactions |

| Personalization | Generic offers | 🤖 AI-driven financial solutions |

| Regulatory Compliance | Established | 📜 Evolving, SAMA-led regulations |

Want to future-proof your banking platform?

Back to top

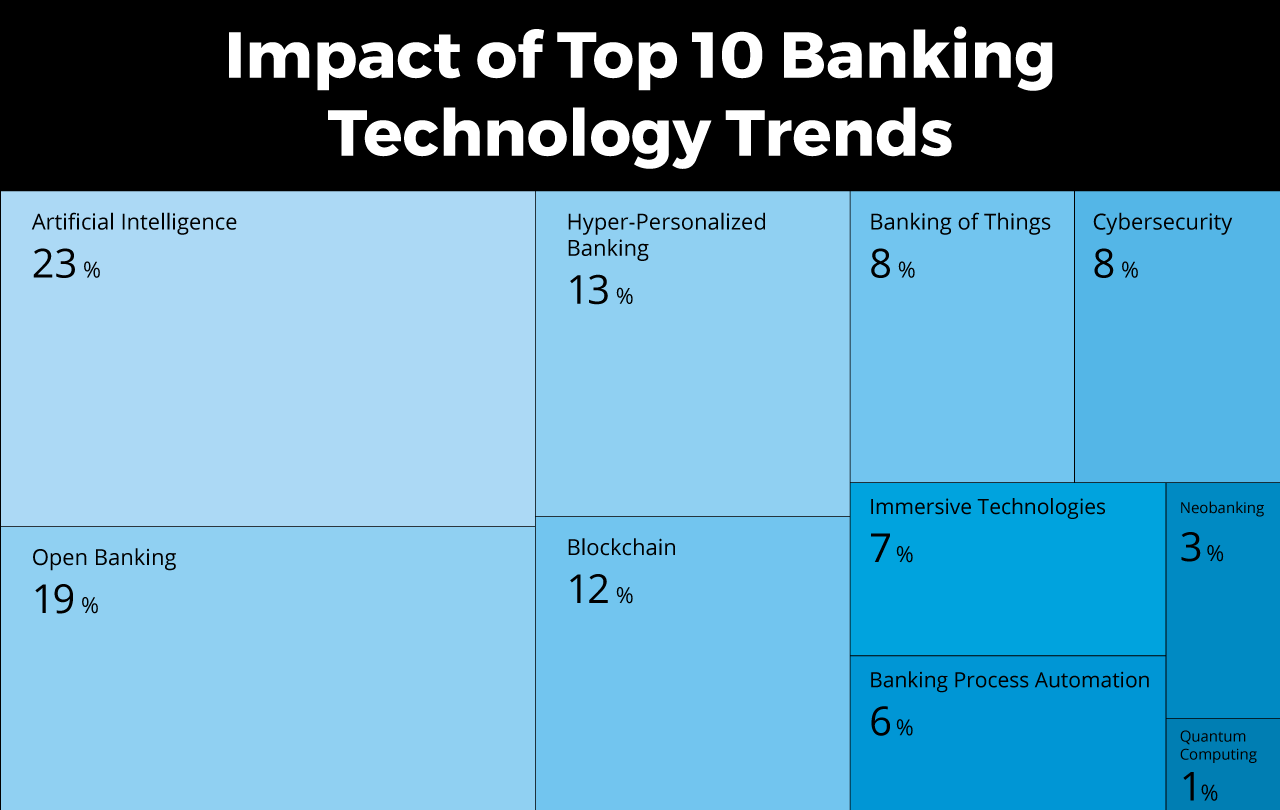

Future Trends and Predictions

Upcoming Technologies

Neobanks, Blockchain, AI, and machine learning are set to further revolutionize open banking. In Saudi Arabia, a pilot project involving blockchain technology aims to enhance the security of financial transactions, promising a safer and more transparent banking experience.

Related: Top Digital Technologies and Trends Impacting Banking and Finance

Regulatory Changes

As open banking matures, we can expect more stringent regulations to come into play. Regulatory bodies like SAMA in Saudi Arabia are already working on frameworks to ensure consumer protection and data privacy. A new set of guidelines is expected to be released by the end of 2023.

Market Trends

The Financial Stability Report 2023 predicts a surge in the adoption of open banking services, especially in developing economies. In Saudi Arabia, consumer awareness campaigns are being planned to further boost the adoption rates.

Related: Learn more about the top 10 future trends in banking

Back to top

The Future of Open Banking in Saudi Arabia

By 2025, open banking is shaping Saudi Arabia’s financial ecosystem, fostering innovation, security, and enhanced user experiences.

AI-driven financial automation is now mainstream.

Fintech growth is accelerating beyond expectations.

Regulatory frameworks are ensuring security & compliance.

Want to integrate open banking solutions?

Author bio: This article was written by Firas Ghunaim, CMO of iSpectra. With over 15 years of experience in digital transformation and fintech marketing, Firas specializes in helping businesses leverage cutting-edge technology to drive financial innovation.

Back to top

FAQs

How does Open Banking improve financial security?

Open Banking enforces stronger authentication & fraud prevention while ensuring API security compliance.

Will Open Banking replace traditional banks?

No. Instead, it enhances traditional banking by enabling seamless digital-first financial experiences.

How do fintechs benefit from Open Banking?

Fintechs gain API-driven access to financial data, enabling personalized banking services.